LGPS Exit Credits Case Studies

On 23 July 2024, we partnered with Burges Salmon to hold a webinar discussing the new discretions in LGPS exit credits and how the discretion granted to the funds might be applied and to analyse practical steps for LGPS participating employers. Our latest bulletin – Bulletin 59 – gives a full account of what was discussed on the webinar, including these case studies.

These examples showcase the situations that can occur for Local Government Pension Scheme’s (LGPS) when deciding how to administer exit credits. Each case study presents it’s own challenges and considerations for both employers and administering parties.

1. The Outsourcer

The employer is participating in the LGPS via an outsourcing contract with the local authority where pension costs are passed through to the authority. The outsourcer is not “on risk” for LGPS pension costs. If they increase it simply charges this increase back to the authority.

In this situation a refund would be very unlikely as the employer has not been on risk during its participation in the LGPS.

2. The Charity

In this scenario the charity is fully on risk, they have participated in the fund for a number of years and have paid substantial deficit contributions historically. In this case, we would expect the fund to pay out the exit credit of £3m.

The charity has been funding the downside risk for a considerable number of years and should therefore be able to benefit and receive the upside exit credit. Whilst the charity might get an exit credit, future expenses might be taken off and the credit might be capped at the level of contributions paid in.

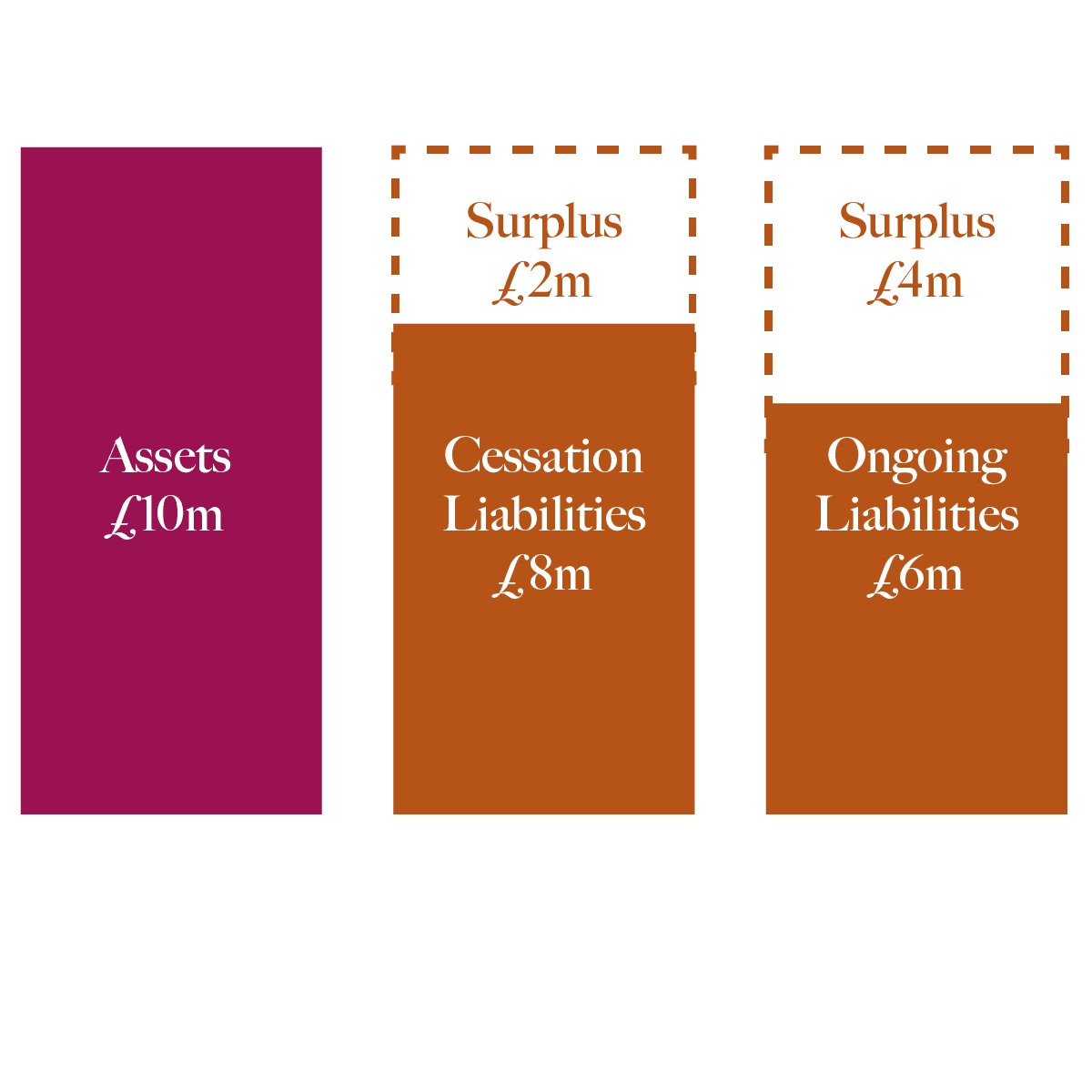

3. The Council Guarantee

Some employers have a guarantee from the Council meaning that that employer only needs to fund the liabilities on an ongoing basis rather than a cessation basis, i.e. fund to £6m of liabilities rather than £8m in the example.

This lower funding basis can sometimes apply on cessation as well. So if this employer is on surplus on both measures on an exit, should they get an exit credit of £4m, £2m or nothing?

How LGPS Guarantee Structures Influence Exit Credit Payments

A guarantee can be structured in any number of ways. At one end of the spectrum, some guarantees are only triggered when the employer fails: when it’s unable to pay or it’s had some kind of insolvency event. Arguably the employer remains on risk in this situation, and therefore should receive an exit credit on cessation.

The other end of the spectrum is that on an exit, the guarantor steps in ahead of the employer, and adopts or subsumes the liabilities of that employer. Or there might be an arrangement whereby the employer leaves on an ongoing basis or anything in between. This does amount to a form of risk sharing or risk transfer, and you therefore might expect the payment of the surplus to be reduced or unlikely. The devil is going to be in detail, and the terms of the guarantee should be carefully scrutinised.

We’ve seen numerous examples of employers in Scottish funds with guarantees where an exit credit has been paid, but it’s been limited to the surplus on a cessation basis rather than an ongoing basis, i.e. £2m rather than £4m in the example.

Have any thoughts?

If you have questions about the new discretions in LGPS exit credits and need further clarification, or you want to explore specific strategies tailored to your scheme, please don’t hesitate to reach out.